Company Registration

2 Weeks

Local Director?

No

Bank Account Opening

4 Weeks

Travel Required?

No

Last Updated on

12 June 2026

Introduction to Canada MSB License

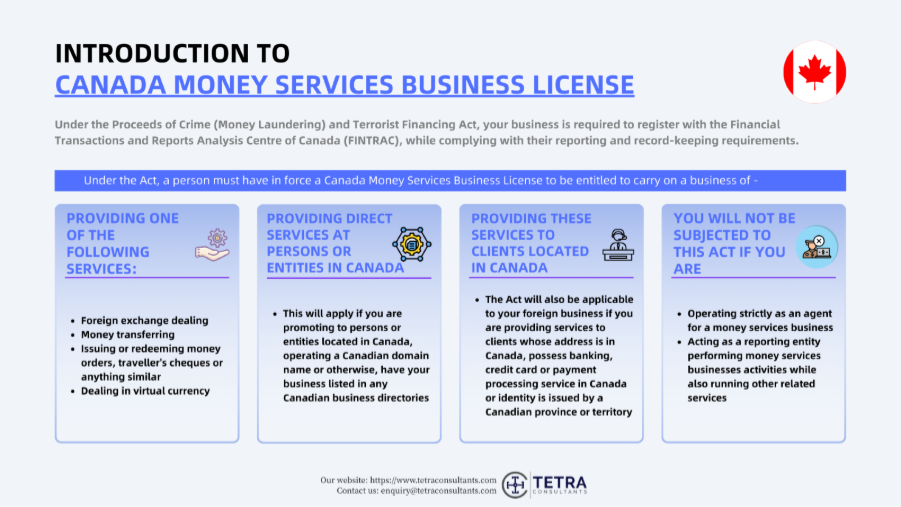

- Canada has now established itself as one of the most recognized jurisdictions for money services businesses (MSBs), especially for companies that are involved in foreign exchange, remittance services, payment processing, and virtual currency operations. The Canadian regulatory model is overseen by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC), which operates under a structured anti-money laundering and counter-terrorist financing framework.

- While a Canadian MSB License is not technically a conventional financial license, it is rather a FINTRAC registration that only allows qualified businesses to legally provide regulated money service activities within Canada or provide services to Canadian residents in certain circumstances.

- In order to get a Canada MSB license, you will first need to register a company in Canada.

- In the past few years, Canada has also become increasingly relevant for cryptocurrency exchanges, OTC trading desks, fintech operators, payment institutions, and international remittance operators looking for a jurisdiction with regulatory clarity and global credibility.

Activities covered under a Canada MSB License

- Foreign exchange dealing– As a Canada MSB, you can participate in the conversion of one fiat currency into another as part of the commercial foreign exchange operations.

- Virtual currency exchange services- You can conduct fiat-to-crypto, or crypto-to-crypto exchange activities involving Canadian customers, as these activities fall within the scope of regulated virtual currency services under Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA).

- Cryptocurrency transfer services- Likewise, you can participate in transmitting virtual currencies on behalf of their clients, which includes wallet-to-wallet transfers or settlement-related transactions.

- Issuance or redemption of money orders- You can also issue, sell, or redeem money orders, traveler’s checks, or similar financial instruments fall within the regulated MSB category.

- Digital wallet operations- Your company can also provide custodial wallet services or facilitate control and transfer of virtual assets.

- International settlement services- You can support international payment settlements, merchant fund transfers, and cross-border financial processing activities.

- Crypto ATM services- If required, your company can also operate cryptocurrency automated teller machines that facilitate virtual currency purchase, sale, or transfer activities via your Canada MSB.

Key advantages of obtaining a Canadian MSB License

International regulatory credibility

- Canada has maintained a mature financial compliance framework that is aligned with the Financial Action Task Force (FATF) standards and international AML expectations. FINTRAC registration further improves the credibility of your business with banks, payment providers, liquidity partners, and other institutional counterparties.

Recognition for virtual currency activities

- Canada formally controls virtual currency service providers under the PCMLTFA framework. This has fostered a clear legal environment for crypto exchanges, OTC platforms, wallet providers, and digital asset businesses.

Transparent registration process

- The registration process for the MSB license is structured and documentation driven. Regulatory policies for Canada MSB License mainly revolve around AML policies, beneficial ownership, transaction monitoring, and compliance governance, which are usually well-defined.

No minimum capital requirement

- Unlike many financial licensing jurisdictions, Canada usually does not impose a fixed minimum capital obligation for MSB registration. This will allow you to easily allocate your resources towards operational development and compliance infrastructure instead of locked regulatory capital.

Centralized regulatory registration

- The Canadian MSB model mainly operates under a federal FINTRAC registration system instead of the fragmented provincial licensing structures for AML supervision. This has further simplified regulatory coordination compared to multi-state licensing environments.

Who needs a Canada MSB License?

- Businesses conducting regulated money service activities in Canada are usually required to register with the FINTRAC before commencing operations. Entities that commonly require Canada MSB registration include:

- Money transfer companies

- Foreign exchange businesses

- Cryptocurrency exchanges

- OTC cryptocurrency trading platforms

- Fintech payment platforms

- Crypto ATM operators

- Payment service provider

- Digital wallet operators

- Remittance companies

- International settlement businesses

- Peer-to-peer payment facilitators

- Foreign entities that serve Canadian customers also fall within the scope of foreign (FMSB) registration requirements, even when the business lacks a physical Canadian office.

- If you are operating your company without appropriate registration, it will face administrative penalties, reputational damage, regulatory restrictions, and possible enforcement action under the Canadian AML legislation.

Legal framework governing the Canada MSB License

- The legal framework that governs the Canada MSB License is mainly centered on Canada’s anti-money laundering (AML), and counter-terrorist financing (CTF) regime. Additionally, in 2026, a new layer of payment safeguard rules took effect.

- The main law that governs Canada MSB is the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), S.C. 2000, c.17.

- The law has imposed obligations on MSBs such as AML/CTF compliance program, KYC/client verification rules, maintenance of records, reporting, and ongoing monitoring

- This law defines what an MSB and a Foreign MSB are in Canada and the activities they can conduct.

- This law has authorized the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) to register MSBs, oversee compliance examinations, and enforce Administrative Monetary Penalties (AMPs) for non-compliance.

- The supporting PCMLTFA Regulations (SOR/2002-184) provide the rules for:

- Client identification and verification methods

- Requirements for beneficial ownership

- Business relationships and ongoing monitoring

- Retention of records (usually to be kept for the last 5 years)

- Report types, timelines, and thresholds

- However, since 2026, Canada has added a strong protective layer through the Retail Payment Activities Act (RPAA), which is overseen by the Bank of Canada. This law is an addition to the FINTRAC registrations and does not replace the PCMLTFA framework. RPAA framework is applicable to the payment service providers that:

- Hold their client funds

- Clear or settle the retail payments

- Initiate payments

- The main focus of this law is on:

- Protecting client funds such as trust accounts, insurance, and guarantees

- Operational risk management that is IT, cybersecurity, and business continuity

- Governance and financial soundness

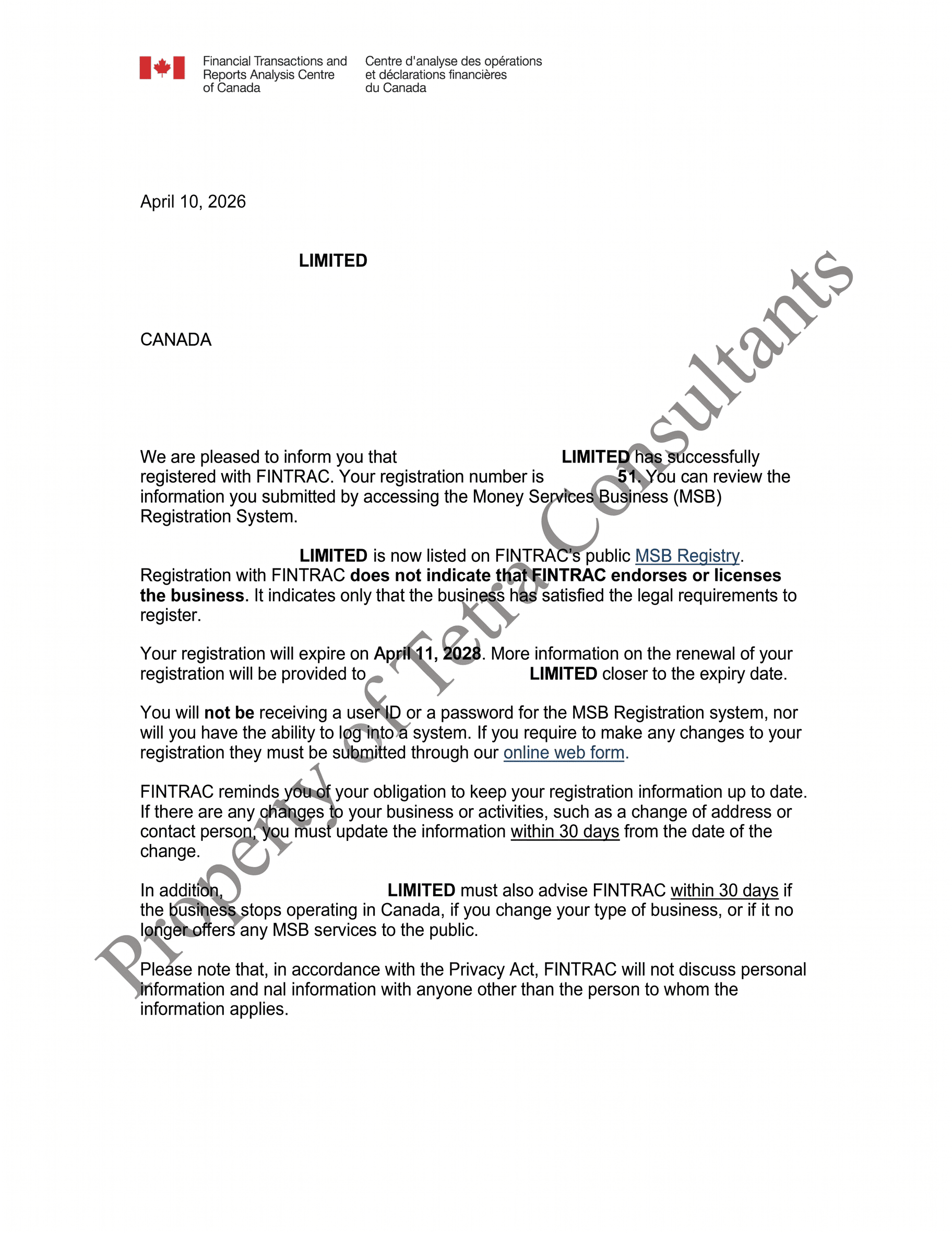

- The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) serves as the main supervisory authority for MSBs in Canada under the PCMLTFA. The role of FINTRAC is to oversee compliance with Canada’s AML/CTF requirements.

- Unlike the traditional licenses that are issued through the prudential approval processes, the Canadian framework requires eligible businesses to register with the FINTRAC before starting regulated money service activities.

- Although there is no government registration fee, FINTRAC has the authority to refuse, suspend, or even revoke the registration where the regulatory requirements are not satisfied.

- The Canadian regime distinguishes between two categories of registrants:

- Money Services Business (MSB)- A business that has a physical presence in Canada along with employees and agents.

- Foreign Money Services Business (FMSB)- A business that does not maintain a physical presence in Canada but directs all the regulated services towards the Canadian customers and conducts transactions involving persons located in Canada.

Requirements for Canada MSB registration

- If you want to register your business as MSBs in Canada, then you should establish an operational as well as compliance framework that satisfies the requirements that have been set out under the PCMLTFA and are related to FINTRAC regulations.

Conducting a regulated MSB activity

- You should engage in one or more regulated money services activities like money transfers, foreign exchange dealing, virtual currency services, or the issuance and redemption of money orders.

- Businesses that do not conduct regulated activities fall outside the scope of MSB registration requirements.

Designation of a compliance officer

- Every MSB is needed to hire a compliance officer who is responsible for overseeing the implementation as well as the effectiveness of the AML/CTF framework.

- The individual should have authority and knowledge to govern the compliance program.

Establishment of a legal business entity

- You should operate legally in Canada through a recognized business structure. Based on the operating model, this may involve a Canadian corporation, partnership, sole proprietorship, or even a foreign entity that is registered as a Foreign Money Services Business (FMSB).

Development of an AML/CTF compliance program

- You need to establish a formal compliance program that is created to identify, evaluate, and mitigate money laundering and terrorist financing risks.

- The program should be personalized as per the nature, size, and model complexity of your business.

Business-wide risk evaluation

- You will have to conduct and document a proper risk assessment that evaluates factors like customer profiles, geographic exposure, delivery channels, products offered, as well as transaction patterns.

- This evaluation further creates the foundation of a strong compliance framework.

Customer identification and verification processes

- You need to implement strong processes to verify customer identities and beneficial ownership information in accordance with the Canadian AML requirements.

- These processes will showcase proper measurements taken to protect customers from risks.

Internal policies and control

- You should establish strong internal controls that govern customer onboarding, transaction monitoring, suspicious activity reporting, record management, and strong regulatory reporting processes.

Beneficial ownership transparency

- The ownership as well as the control structure of your business should be clearly identifiable. FINTRAC expects your business to showcase transparency regarding directors, shareholders, ultimate beneficial owners, and individuals who exercise major control over the business entity.

Operational readiness

- Your company should be able to show that it possesses the operational infrastructure that is required to conduct regulated activities responsibly.

- This consists of proper governance arrangements, internal processes, and systems that are capable of supporting regulatory compliance.

Accessibility for regulatory supervision

- You should be capable of responding to the FINTRAC inquiries, examinations, and compliance reviews.

- Regulatory authorities should be able to recognize responsible individuals and evaluate the effectiveness of the compliance framework when needed.

Ongoing compliance obligations for MSBs

- After registering with FINTRAC, MSBs in Canada are required to maintain ongoing compliance with the anti-money laundering and counter terrorist financing framework of Canada.

- These obligations go beyond the initial registration and create a critical part of the regulatory regime under the PCMLTFA.

AML/CTF compliance program

- Your MSB should maintain a documented compliance program that is based on the nature and risk profile of your business. This usually includes:

- Written AML/CTF policies and processes

- Appointment of a designated compliance officer

- Internal governance and strong oversight mechanisms

- Periodic review and improvement of compliance controls

Customer due diligence (CDD)

- Your company needs to continuously evaluate and monitor customer relationships throughout its life cycle. This usually includes:

- Identity verification measures

- Verification of beneficial ownership

- Ongoing monitoring of customer activities

- Better due diligence for higher-risk customers

Recordkeeping obligations

- Your company will have to maintain accurate records in order to support customer identification, oversee transaction monitoring, and fulfill regulatory reporting requirements. The required records usually consist of:

- Customer identification records

- Information about beneficial ownership

- Transaction records

- Compliance program documentation

- Regulatory reporting records

Regulatory reporting requirements

- Your MSB should submit multiple reports to FINTRAC when prescribed thresholds or reporting triggers are fulfilled. These may consist of:

- Suspicious transaction reports (STRs)

- Terrorist property reports (TPRs)

- Large virtual currency transaction reports (LVCTRs)

- Large cash transaction reports (LCTRs)

Risk assessment and monitoring

- Your MSB is expected to maintain a documented risk-based approach to ensure proper compliance and continuously evaluate potential exposure to money laundering and terrorist financing risks. This usually consists of:

- Customer risk

- Delivery channel risk

- Product and service risk

- Geographic risk

- Emerging financial crime threats

Employee training

- Your staff who are a part of your business should get ongoing AML/CTF training in order to ensure that they can easily understand their compliance responsibilities. Training programs usually cover:

- AML/CTF regulations

- Internal compliance processes

- Identification of suspicious activity

- Reporting obstacles

- Regulatory developments

Beneficial ownership maintenance

- You should take reasonable measures to ensure that the ownership information of your business stays accurate and up to date. This consists of:

- Monitoring changes in the ownership structure

- Updating beneficial ownership records

- Maintaining transparency regarding individuals who are in control of the business operations

Independent compliance review

- The effectiveness of your business’ compliance program should be periodically evaluated through an independent review. The review should assess:

- Sufficiency of internal controls

- Areas that require corrective action

- Reporting procedures

- Effectiveness of AML processes

FINTRAC examinations and audits

- Your registered business entity is subjected to regulatory examinations that are conducted by FINTRAC. During this examination, the authority will review:

- AML policies and processes

- Customer due diligence processes

- Transaction monitoring systems

- Reporting practices

- Compliance governance framework

Changes in reporting material

- You will also have to notify FINTRAC regarding significant changes that affect their registration or business operations. This includes:

- Changes in the control or ownership of the business

- Appointment of a new compliance officer

- Changes to the business activities

- Changes to contact or registration information

Difference between MSB and FMSB registration

| Criteria | Money Service Business (MSB) | Foreign Money Service Business (FMSB) |

| Business Presence | It is mandatory for MSB to maintain a place of business in Canada. This usually consists of a Canadian corporation, office branch, employees, or agents that are operating within Canada. | FMSB does not maintain a physical office in Canada but offers regulated money services to individuals located in Canada. |

| Target Market | MSBs mainly serve customers within Canada, although international operations can also be conducted. | FMSBs targets Canadian customers outside of Canada and conducts transactions that involve Canadian residents. |

| Compliance officer | MSB is required to hire a designated compliance officer who is responsible for AML oversight. | FMSBs are required to designate a responsible individual who can oversee compliance with the Canadian AML obligations. |

| Compliance program | MSBs should establish and operate a compliant AML/CTF program aligned with FINTRAC requirements. | FMSBs are subjected to substantially similar AML/CTF compliance obligations despite operating outside of Canada. |

| Prime Regulatory Focus | Regulation of money service activities that are conducted within Canada. | Regulation of cross-border money service activities that are directed at the Canadian market. |

Step-by-step process to obtain a Canada MSB License

Step 1- Evaluate the business model and regulatory scope

- The first stage consists of determining whether your proposed business activities are falling within the scope of regulated money services business activities under the PCMLTFA framework.

- You need to conduct a regulatory evaluation of the proposed activities, target markets, and transaction flows.

- Determine whether the registration of your business should be done as a domestic MSB or a Foreign Money Services Business (FMSB).

- You need to recognize any additional regulatory considerations relating to virtual currencies, payment services, or cross-border transactions.

Step 2- Establish the business structure

- Before initiating the registration procedure, your business should operate through an appropriate legal structure capable of supporting the regulated activities.

- You need to incorporate a Canadian company and get a Business Number (BN) from the Canada Revenue Agency (CRA).

- You have to finalize the ownership structure, governance arrangements, along with the management framework.

- You also need to ensure that the directors, shareholders, and ultimate beneficial owners can be clearly recognized and disclosed.

Step 3- Develop the AML/CTF compliance framework

- A strong compliance framework is a fundamental requirement of the Canadian regulatory regime and should be established before registration.

- You have to prepare AML and counter-terrorist financing policies that are tailored to the business model and risk profile.

- You also have to hire a qualified compliance officer who is responsible for overseeing the regulatory obligations.

- Lastly, you need to create customer due diligence, transaction monitoring, sanctions screening, and reporting processes.

Step 4- Conduct a business-wide risk evaluation

- Canadian regulations require your business to take a risk-based approach to AML compliance.

- You need to evaluate customer, geographic, product, and delivery channels along with risks associated with the proposed operations.

- You also need to recognize potential money laundering and terrorist financing vulnerabilities.

- Lastly, you need to implement risk mitigation measures appropriate to the level of identified exposure.

Step 5- Prepare registration information and supporting disclosures

- The registration application should accurately showcase the operational structure and compliance arrangements of your business.

- You need to compile all the information related to your business activities, ownership structure, and key personnel.

- You also have to prepare disclosures about directors, beneficial owners, and compliance contacts.

- Verify that all the information submitted is consistent with your business model and compliance framework.

Step 6- Submit the FINTRAC registration application

- Once your business structure and compliance program have been established, the registration application can be submitted to FINTRAC for review.

- You need to complete the registration process through FINTRAC’s designated registration platform.

- You have to provide all the information related to your business and regulated financial activities.

- Lastly, you need to respond to any requests for clarification or additional document requests during the review process.

Step 7- Implement operational and compliance controls

- Following the business registration, you need to ensure that your business’ compliance framework is fully operational before starting the regulated activities.

- You also have to implement clear customer onboarding, verification, and transaction monitoring systems.

- Establish strong internal reporting channels and recordkeeping processes.

- Lastly, you need to conduct employee training on AML obligations and regulatory requirements.

Step 8- Maintaining ongoing regulatory compliance

- After registering with FINTRAC, your business entity should follow ongoing compliance obligations that should be maintained throughout the life of the business.

- You need to monitor customer relationships and transactions regularly.

- You have to submit regulatory reports where the reporting thresholds or suspicious activity triggers are met.

- You must periodically review and update the compliance policies, risk evaluations, and internal controls to stay aligned with the regulatory expectations.

Comparison of Canada with alternative MSB jurisdictions

| Criteria | Canada (MSB/FMSB) | Lithuania (MiCA CASP/Fintech) | United States (MSB + State MTLs) | Poland (CASP/ Fintech Framework) |

| Primary regulator | FINTRAC | Bank of Lithuania | FinCEN and individual State Regulators | Polish Financial Supervision Authority and competent authorities |

| Regulatory framework | PCMLTFA and FINTRAC regulations | MiCA, EU AML Framework, Travel Rule requirements | Bank Secrecy Act (BSA), FinCEN Regulations, State Money Transmission Laws | MiCA and EU AML Framework |

| Regulatory model | Registration-based AML supervision | Full authorization and licensing framework | Federal registration combined with multiple state licenses | EU authorization framework |

| Physical presence requirement | Physical presence is needed for domestic MSBs, not for FMSBs | Local substance and management presence are usually expected | Often requires local registrations and state-specific compliance arrangements | Local operation presence is expected based on the business model |

| Regulatory complexity | Moderate | Moderate to high | High | Moderate |

| Application complexity | Relatively straightforward after the compliance infrastructure is established | Detailed authorization process consisting of governance risks, management, and operational controls | Usually complex because of multiple-state level filings and approvals | Moderate based on the business activities |

Timeline and cost considerations

- Company registration: 2 weeks

- MSB license application preparation (business plan, AML policy, application forms): 2 weeks (parallel with company registration)

- FINTRAC application submission & case officer assignment: 4 to 8 weeks

- FINTRAC review (interview, queries, additional documents) & MSB approval: 4 to 6 weeks

- RPAA registration & submission: 1 week

- Corporate bank account opening (operational + segregated accounts): 4 weeks (runs parallel post-submission/approval stage)

- Overall timeline: approximately 12 to 17 weeks

- The cost of a Canadian MSB License at Tetra Consultants is based on an entirely transparent, comprehensive, and package-based price structure that meets all major requirements since there are no fees or charges directly applied by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC).

- Our package usually consists of consultation, advisory fees, corporate registration costs, anti-money laundering (AML)/know-your-customer (KYC) procedures, compliance program development, and further post-registration assistance.

Evidence

How can we help in obtaining Canada MSB License?

- Tetra Consultants works as your advisor and trusted partner in your business expansion and payment license application. With our own team of lawyers, licensing specialists, compliance team, and accountants, we tell our clients what they need to know, instead of what they want to hear. Most importantly, we are known for being a one-stop solution for our valued clients. Here are the reasons why our clients choose us:

- We have more than 10 years of experience in helping clients with financial licensing, regulatory reporting, and international business expansion across various jurisdictions

- A dedicated team of lawyers, compliance professionals, incorporation specialists, accountants, and tax advisors who support you throughout the engagement

- End-to-end support that covers company incorporation, regulatory registration, compliance framework development, and operational setup

- Assistance with corporate bank account opening services through our vast network of banking partners and financial institutions

- Preparation of AML/KYC policies, risk assessment frameworks, and internal compliance procedures that are aligned with Canadian regulatory requirements

- We provide ongoing regulatory compliance consulting services to help businesses maintain compliance with FINTRAC obligations following registration

- To get a Canada MSB License, contact us, and our team will get back to you in 24 hours.

![]()

As Featured In Yahoo Finance

Tetra Consultants appoints Lester Mok as Director to strengthen global business expansion and reinforce the firm’s commitment to delivering international business advisory services worldwide.

Managing Director, Tetra Consultants

Lester Mok

Lester Mok oversees Tetra Consultants’ global operations and financial licensing team. He brings a strong background in international business law, regulatory strategy, and corporate finance shaped by his years of hands-on experience. With deep expertise in cross-border business expansion and financial licensing compliance, he has helped clients establish and grow their presence in multiple jurisdictions while navigating complex regulatory requirements. Over the years, he has been featured in multiple press releases from Yahoo Finance and Fidelity.