Company Registration

2 Weeks

Local Director?

No

Bank Account Opening

4 Weeks

Travel Required?

No

`

Table Of Contents

Canada MSB License (Money Services Business) in 2026

- Tetra Consultants’ legal team and licensing specialists can help you to obtain the Canada Money Services Business License, which falls under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, as well as the updated regulations from the Financial Transactions and Reports Analysis Centre of Canada, which came into effect in 2025. The Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) is intended to prevent crime, including financial failures and related offenses.

- The enhancements to the law have provided the ability to monitor money services businesses better than ever before by creating higher standards of registration, reporting, and compliance to combat transnational threats, including money laundering and terrorist financing, while enhancing protection against new risks (i.e., fintech’s and cryptocurrencies).

Introduction to Canada MSB License

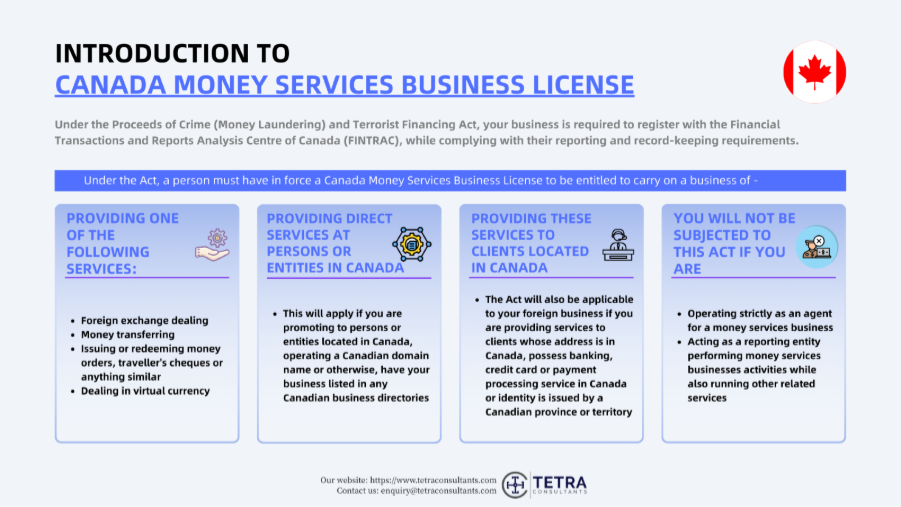

- The MSB registration in Canada allows businesses to provide currency exchanges, money transfers, remittances, and cryptocurrency services across Canada in a licensed manner. Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) oversees the MSB registration in Canada and is essential for providing access to Canada’s fastest-growing FinTech sectors, which handle billions in annual transactions. At the same time, it ensures high anti-money laundering standards to safeguard both the customer’s money and a business’s ability to operate legally and safely.

Who needs Canada MSB License in 2026

Money transfer providers

- Companies providing domestic or international money transfer services to or from Canada through peer-to-peer services.

Foreign exchange companies

- These companies provide foreign exchange services, including fiat-to-fiat foreign exchange services and multi-currency payment gateways catering to Canadian-based customers.

Payment service providers (PSPs) and payment processors

- Organizations that process payments for merchants, issue/redeem payment-function cards, or process payment intermediation services related to Canadian-based payers or payees.

Crypto asset (virtual assets) service providers

- Crypto asset exchanges, over-the-counter markets, as well as companies facilitating conversion and transfer of crypto assets on behalf of Canadian-resident customers.

Crypto asset custodians or managed wallets

- Companies providing custodian or managed wallets, along with crypto asset custodianship, that issue/redeem/distribute virtual asset-based payment functions for Canadian customers.

Money order and travellers’ check issuers and redeemers

- Issuers and redemption companies of money orders, travellers’ checks, stored value cards, and similar instruments for Canadian-based individuals or organizations.

Crowdfunding and investment platforms collecting fiat or cryptocurrency

- Crowdfunding and investment platforms raising or distributing fiat or crypto funds for investments in Canada may fall under MSB Regulations in Canada depending on their payment function role.

Entities outside Canada that serve customers in Canada

- Overseas MSB or Fintech that takes in clients with a Canadian address, uses Canadian banking institutions for payment processing, or conducts Canadian ID verification needs to register as an MSB/FMSB in Canada.

Crypto ATMs and Crypto Kiosks providing Cash-Out Services

- Cryptocurrency ATMs or kiosks are involved in crypto-to-cash exchange transactions anywhere within Canada.

Fintechs and Embedded-Finance firms offering money services and business services

- Every fintech startup, neobank-like service, or embedded-finance solution that provides financial services to Canadian citizens is required to obtain authorization as a Money Services Business (MSB) in Canada.

New 2025/2026 Bank of Canada (RPAA) Requirements

Mandatory Retail Payment Activities Act (RPAA) registration for Money Services Business (MSB) license holders in Canada

- RPAA refers to Retail Payment Activities Act, which is a Canadian federal law that supervises payment service providers (PSPs). Bank of Canada is the primary regulator responsible for the supervision.

- MSB registration holders in Canada, acting as PSPs, are mandated to register with the Bank of Canada via the PSP Connect portal by September 7, 2025, for the purpose of compliance in 2026.

- Tetra Consultants is proficient in assisting your company to attain RPAA registration with Bank of Canada once your MSB registration in Canada is successful.

Retail Payment Activities Act (RPAA) impacting Canada MSB

- RPAA regulates MSB registration in Canada, which provides payment services, including fund holding, EFT initiation/authorization, payment account maintenance, and clearing/settlement for Canadian end-users. This is in addition to traditional remittance and forex services.

Application fees and exemptions

- Application fees are non-refundable, and banks and credit unions are exempt from the fees. The registration is a must for Money Services Business (MSB) in Canada that handle retail payment services.

Risk management and safeguards

- Full risk management systems, end-user fund protection systems, reporting systems for incidents, and operational resilience systems that meet Bank of Canada standards.

RPAA complements FINTRAC MSB rules

- RPAA builds on FINTRAC’s rules for money services businesses, providing a multi-layered solution for money services businesses looking to enter Canada’s payment market.

Seamless MSB + RPAA setup

- Tetra Consultants’ team of lawyers and licensing specialists is happy to assist our international clients with attaining a Money Services Business (MSB) in Canada from FINTRAC as well as RPAA registration with the Bank of Canada.

PSP Criteria under RPAA Registration:

- The Payment Service Providers are required to register with the Bank of Canada in case you are involved in the provision of payment services such as the collection of funds, transfer, redemption, or storage of funds that exceed an annual volume of CA$ 10 million or are involved in cross-border transactions for Canadian clients.

Exclusions under RPAA Registration:

- Banks, foreign banks, insurance companies, credit unions, intermediaries acting on behalf of the registered PSP, incidental payment services with regard to the volume threshold, or technology providers are excluded.

FINTRAC reporting thresholds in 2026

Large Cash Transaction Reporting (LCTR):

- Submit a report to FINTRAC within 15 calendar days for transactions above CA$10,000. It should include the transaction date, amount, parties involved, type of transaction, and business details of the Money Services Business (MSB) in Canada. Records should be maintained for 5 years to comply with Canada’s MSB License.

Suspicious Transaction Reporting (STR):

- Submit a Suspicious Transaction Report to FINTRAC immediately if you suspect any money laundering or financing of terrorism in accordance with PCMLTFA. It should include details of your company personnel detail, transaction details, amount, etc.

Terrorist Property Reporting:

- Submit a report to RCMP ASAP if you suspect any terrorist-owned properties. It should include details of properties and suspect details. It is critical for Canada’s MSB License holders in 2026.

Cross-Border Currency Reporting:

- Submit a declaration form E677 to CBSA for transactions above CA$10,000. It includes reporting of currency and/or monetary instruments. Failure to comply may result in seizure and fines for Money Services Business (MSB) in Canada.

Large Virtual Currency Transaction Reports:

- MSBs for virtual currencies shall file reports for transactions involving CA$10,000+ in cryptocurrencies to FINTRAC within 5 business days. Information to include is date, amount, exchange rate, originator/recipient details. Record retention for 5 years in accordance with PCMLTFA updates issued in 2020 and later.

Electronic Funds Transfer (EFT) Reports:

- EFTs involving CA$10,000+ shall be filed to FINTRAC within 5 days. Information to include is sender/receiver details, accounts, and references. Record retention for 5 years for the Money Services Business (MSB) in Canada.

Travel Rule for Wire Transfers:

- MSBs shall include originator/beneficiary name, address, and account details for wire transactions involving CA$1,000+. Mandatory record retention for 5 years in accordance with PCMLTFA for MSBs.

Step-by-step process to obtain a Canada MSB License?

Step 1: Register a Canadian company

- In the first step, we will undertake the company registration in Canada with the relevant federal or provincial authorities. Our firm will be responsible for securing a local address, nominee director (if needed), and company secretary services. The whole process will take about 2 weeks.

Step 2: Preparation of compliance documents & appointment of compliance officer

- Next, we will undertake preparation of all necessary compliance documents, which include the business plan, AML/CTF compliance program, internal policies, framework of training of employees, and risk assessments under regulations of FINTRAC and the PCMLTFA. Alongside, we will help your company to appoint a competent Canada compliance officer.

Step 3: Appointing a representative from Canada (if necessary)

- If necessary, we will appoint a suitable representative from Canada for your business who will be capable of receiving any communication from the government.

Step 4: Start pre-registration using FINTRAC website

- Additionally, we will give you access to FINTRAC’s website to facilitate the pre-registration process. All necessary information, including the business number, e-mail address, and company identification information, will be included to receive your first level of approval.

Step 5: Submit complete MSB registration application

- Next, a complete MSB registration application will be filed. Bank account information (if available), details of the compliance officer, number of employees, information regarding company incorporation, and police background check (for foreign corporations) will be included. Tetra Consultants can also facilitate English translation of documents, if needed. The firm helps your business to grow and manage your company’s compliance.

Step 6: RPAA registration

- After completing or initiating MSB registration, we will examine your activities to determine if you require RPAA registration through the Bank of Canada.

Step 7: Corporate bank account opening

- We will provide help for corporate bank account opening with reliable Canadian banks or other financial organizations across the globe. After gaining approval, the account will be activated for operational purposes.

Cost to obtain Canada MSB license in 2026

- Our Canada MSB Licensing service for 2026 by Tetra Consultants is based on an entirely transparent, comprehensive, and package-based price structure which meets all major requirements since there are no fees or charges directly applied by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC).

- Our package usually consists of consultation, advisory fees, corporate registration costs, anti-money laundering (AML)/know-your-customer (KYC) procedures, compliance program development, and further post-registration assistance.

- The government-related expenses can include the provincial license (e.g., at a rate of approximately CA$ 1,000 to 2,500 per category) and other related assessments like Bank of Canada-style yearly fees (CA$ 2,500), whereas the registration with the federal authority (FINTRAC) is free of any government charges upfront. Notably, there are no hidden or extra costs imposed by us.

Timeline to obtain Canada MSB license in 2026

- Company registration: 2 weeks

- MSB license application preparation (business plan, AML policy, application forms): 2 weeks (parallel with company registration)

- FINTRAC application submission & case officer assignment: 4 to 8 weeks

- FINTRAC review (interview, queries, additional documents) & MSB approval: 4 to 6 weeks

- RPAA registration & submission: 1 week

- Corporate bank account opening (operational + segregated accounts): 4 weeks (runs parallel post-submission/approval stage)

- Overall timeline: approximately 12 to 17 weeks

What do you need to know about the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) in 2026?

- It is essential to understand the needs of the PCMLTFA regulations in Canada, which provide the foundation for the regulations governing MSB companies. The company will operate within the law when it is compliant with this regulation. Thus, here are the following important sections:

Section 11.1:

- Mandatory FINTRAC registration for all forex, remittances, and crypto services, which will be your first step in MSB regulations.

Section 9(1):

- Client verification for CA$3,000+ forex/negotiables, CA$1000+ remittances for KYC is essential.

Section 7:

- Immediately file Suspicious Transaction Reports when money laundering suspicions occur, there will be instant threat detection.

Section 12 and 48:

- LCTR/EFT reporting for transaction CA$10,000+ within 5-15 days, also, record to be kept for 5 years.

Section 73.1 to 73.16:

- AMPs up to CA$20 million for non-compliance and also some serious financial repercussions may occur.

Section 74:

- Criminal Penalties for non-compliance are a CA$2 million fine with a 10 year in prison for wilful offenses.

MSB vs. FMSB in Canada in 2026

| Aspect | MSB (Money Services Business) | FMSB (Foreign Money Services Business) |

| Geographic Scope | Must have place of business in Canada (incorporation, physical location, employees/agents/branches). | No place of business in Canada (not incorporated, no physical location/employees/agents there). |

| Client Targeting | Serves clients in Canada (and potentially internationally). | Directs services at and provides to persons/entities in Canada (e.g., marketing, Canadian clients with residential ties). |

| Authorized Activities | Identical: foreign exchange dealing, remitting/transmitting funds (incl. invoice payments, payment services), issuing/redeeming money orders/travellers’ cheques, virtual currency dealing/transfer, crowdfunding platforms, armored car services, cheque cashing, private ATM acquirer services. | Same as MSB. |

| Regulatory Body | Registered with and supervised by FINTRAC under PCMLTFA. | Register with FINTRAC under PCMLTFA (no direct issuance, but compliance required). |

| Compliance Program | Mandatory: Appoint compliance officer, AML/CTF policies, risk assessment, customer due diligence (KYC), ongoing monitoring, beneficial ownership checks, PEP determinations. | Mandatory: Same as MSB (robust AML/CTF program tailored to operations). |

| Reporting Obligations | Submit STRs, LCTRs ($10k+ cash), LVCTRs, EFTRs ($10k+), TPRs; 24-hour rule applies. | Same as MSB. |

| Record Keeping | Retain client ID, transaction records (min. 5 years). | Same as MSB. |

| Agent/Mandatary Rules | Verify eligibility, criminal record checks (CEO, directors, 20%+ owners) before/every 2 years; retain 5 years. | Same as MSB (if applicable). |

| Public Registry | Listed on FINTRAC public MSB registry post-registration. | Listed similarly as registered FMSB. |

Banking issues in Canada MSB License in 2026

Challenges of corporate banking accounts opening for MSBs

- Both Canadian and foreign banks “de-risk” money service businesses and thus deny access to banking services. The consulting firm Tetra has its own team of partner financial organizations with which it matches MSB customers and finds banking institutions more tolerant towards MSB and able to process high amounts of transactions.

More stringent KYC & AML regulations imposed by banks

- Banks need detailed information on the customer’s KYC and AML manuals, transaction monitoring procedures, and FINTRAC compliant internal control measures. Tetra consultants provide all required information to banks, such as AML/CFT policies, governance framework, and risk assessment.

Non-resident founders and no physical presence in Canada

- Banks often refrain from taking on MSB businesses with non-resident founders who have no Canadian office or local director. Tetra Consultants assists in the creation of adequate local substances and explains how to present an MSB to banks in such a way that non-resident ownership is properly documented and low risk.

Linking MSB license with RPAA and payment‑system access

- Certain activities are now regulated by the Bank of Canada under the Retail Payment Activities Act (RPAA). Banks expect MSBs to be in line with the requirements of both FINTRAC and RPAA. Tetra Consultants’ experts take care of all relevant issues regarding the connection between the two regulators and help clients contact banks and the payment system.

Perception and reputation risk in the high-risk sector

- The traditional Canadian banks generally consider MSBs, particularly the ones that operate in cryptocurrencies, as high-risk businesses, thus providing unfavourable account conditions or rejecting them. The team at Tetra Consultants presents the company as an MSB that operates in accordance with the laws, regulations, and best practices, relying on the successful experience of their clients as well as proper documentation.

Multi-jurisdictional and multi-banking approach

- MSBs often require having several accounts in different jurisdictions (Canada/ Europe/the United States/overseas). Tetra Consultants provides a multi-bank solution, ensuring primary accounts opened in Canada and additional correspondent accounts or relationships with an EMI/EMI equivalent in other jurisdictions.

Looking to obtain Canada MSB License

- Tetra Consultants works as your advisor and trusted partner in your business expansion and payment license application. With our own team of lawyers, licensing specialists, compliance team, and accountants, we tell you what you need to know, instead of what you want to hear. Most importantly, we are known for being a one-stop solution for our valued clients.

- In addition, Tetra Consultants can also assist with attaining other offshore financial licenses depending on your long-term business goals. Also, our local team in Canada is more than happy to assist with your engagement

- Contact us to find out more about how to secure a Canada MSB License to conduct Money Services Businesses. Our team of experts will revert within the next 24 hours.

FAQs

How do you report to FINTRAC?

What are the deadlines for various reports?

What happens to reports made?

Do fees apply during reporting?

Do incomplete suspicious transactions require reporting?

What documents are required for a Canada MSB license?

What are the penalties for non-reporting under a Canada MSB license?

What are the requirements for record-keeping for a Canada MSB license?

What are some of the most common challenges to obtaining a Canada MSB license in 2026?

How long does it take?

Author

Sharma Prabakaran

Sharma Prabakaran is the Head of International Business Advisory at Tetra Consultants. With over 15 years of professional experience, he specialises in international business setup, accounting and tax advisory, and cross-industry SME engagements. His expertise encompasses end-to-end project management, ranging from company incorporation and corporate bank account establishment to ongoing annual accounting and tax compliance.