Company Registration

1 Week

Local Director?

No

Bank Account Opening

4 Weeks

Travel Required?

No

UK EMI license

- Tetra Consultants can assist you in obtaining a UK Electronic Money Institution (EMI) license from the Financial Conduct Authority (FCA). Our team of lawyers, legal experts and regulatory consultants helps you through the entire Electronic Money Institution authorization process, ensuring that your application is well-structured.

- We also ensure that your business plan is well-written, and your application meets the Electronic Money Institution license requirements set by the Financial Conduct Authority, including those on capital, corporate governance, anti-money laundering/combating the funding of terrorism, and information technology, among others.

- Gaining access to an Electronic Money Institution license allows your business to successfully operate in the issuance of electronic money, the execution of payment transactions, and the delivery of innovative payment services in the UK, as well as in the entire European Economic Area in the case of an Authorised Electronic Money Institution license.

What is an electronic money institution?

- An electronic money institution, abbreviated as EMI, is a financial entity that is authorised to conduct the business of issuing electronic money as well as provide payment services to customers. EMIs store money in electronic form, like e-wallets or virtual accounts, and facilitate payments, transfers, as well as card transactions without the ability of the EMI to act as a bank, lending money to customers.

- The key financial authority for a UK EMI license in 2026 will be the Financial Conduct Authority (FCA), who will oversee and regulate electronic money institutions under the UK’s financial services legislation.

- The financial legislation and instruments for a UK EMI license will include the Electronic Money Regulations 2011 (EMR), the Payment Services Regulations 2017 (PSR 2017), implementing the revised Payment Services Directive (PSD2), the UK’s AML/CTF legislation under the Money Laundering Regulations (the UK has not adopted 6AMLD), and the level of regulation from the FCA in respect of prudential capital (minimum of €350,000), safeguarding audit (annual audit of safeguarding processes), transaction monitoring/sanctions screening, and strong customer authentication (SCA).

- Additionally, forthcoming regulations will place emphasis on digital operational resilience, including robust API/SDK integration and IT security controls for EMI-level payment infrastructure.

- For firms who are serving EU clients or operating group entities within the European Union, the EU Digital Operational Resilience Act (DORA) will also be relevant. While DORA is not directly applicable under UK law, UK-based EMIs with EU exposure should ensure compliance with DORA requirements when serving EU markets or interacting with EU-regulated entities

What are the regulatory requirements for obtaining an EMI license in the UK in 2026?

- The applicant has to be a company incorporated in the UK under the Companies Act, with its registered office in the United Kingdom.

- The business has to have at least an initial capital of €350,000 (or the equivalent in other currencies) if the EMI is an Authorised EMI; Small EMIs, on the other hand, have lower capital requirements, but they are restricted to operating within the UK.

- The EMI has to ensure the safe storage of client money in client bank accounts that are segregated from the EMI’s own money, or through an insurance model, as per the Electronic Money Regulations (EMR).

- The EMI has to have sufficient own resources as well as an effective capital adequacy model, taking into account ongoing business risks.

- A business plan has to be developed by the company, including the business plan, product plan, target markets, revenue, cost, as well as capital adequacy projections, at least for the first 3-5 years.

- The EMI shall have sound governance, internal controls, and risk management systems, including operational, IT, and credit/liquidity risks, that are acceptable to the FCA.

- The operator shall have an effective AML/CFT system that covers aspects of KYC, CDD, TM, SS, and SAR.

- The EMI shall have sound IT infrastructure, including data protection that meets the UK GDPR and FCA security requirements.

- The firm shall have professional indemnity insurance in place if it is seeking to provide Account Information Services (AIS) or Payment Initiation Services (PIS).

- The applicant shall provide detailed documentation, including constitutional documents, ownership structure, forecasted financial statements, risk management policies, AML/CFT manuals, etc.

Key person requirements

- The EMI must have at least one director or executive with day-to-day responsibility for the e-money business, and there must be no restriction on their place of residence.

- The EMI must have a compliance officer with experience and expertise in financial services regulation and AML/CFT.

- The EMI must have a Money Laundering Reporting Officer (MLRO) with experience and expertise in AML/CFT.

- Directors and individuals with significant influence (PSCs/PEPs) must be of good reputation, have no criminal record or adverse media reports, and must pass fit and proper tests at FCA levels.

- The EMI must ensure that no disqualified person is involved in the management or ownership of the EMI.

Who is exempted from getting a UK EMI license?

- Payment services provided by banks and credit institutions already authorised under the FSMA are exempt from the need to obtain a UK EMI license.

- Small EMI (SEMI) business below specified thresholds may be eligible for the lighter regime of registration only instead of full EMI authorisation.

- Some exempt persons defined by the Financial Services and Markets Act 2000 (Exemption) Order (as amended by the 2026 amending regulations) are exempt from the general prohibition on carrying out E-money business.

- Intra-group or ancillary e-money business, such as closed loop schemes used within a single corporate group, may be outside the scope of the need to obtain a retail-focused EMI license.

- Some forms of non-commercial or low-risk payment handling business (for example, agent-only or back end only infrastructures) may be considered as exempt or TFE by FCA-level guidance in the 2026 regime.

What are the types of EMI?

There are two main types of e-Money institutions in the UK:

Authorised EMI (AEMI)

- An AEMI is a fully licensed EMI, authorised by the FCA, permitted to issue e-money and offer various payment services without any restriction on volumes, as long as it has a minimum initial capital of €350,000, as well as full safeguarding and anti-money laundering requirements.

Small EMI (SEMI)

- A small EMI has a lighter regime with lower thresholds for average outstanding volumes of e-money and related payment volumes, permitted to operate only in the UK and is appropriate for startups or small-volume operators, which can then become AEMIs if they exceed these thresholds.

Why do you need a UK EMI license?

- A UK EMI license is a fantastic choice in 2026 as it will provide a fintech or a payment business with a legal license to provide electronic money services and issue e-money in the United Kingdom, with a clear regulatory framework under the FCA. It is a license that will promote innovation in digital wallets, borderless payments, and embedded finance, with credibility with partners, banks, and customers in a high-trust location.

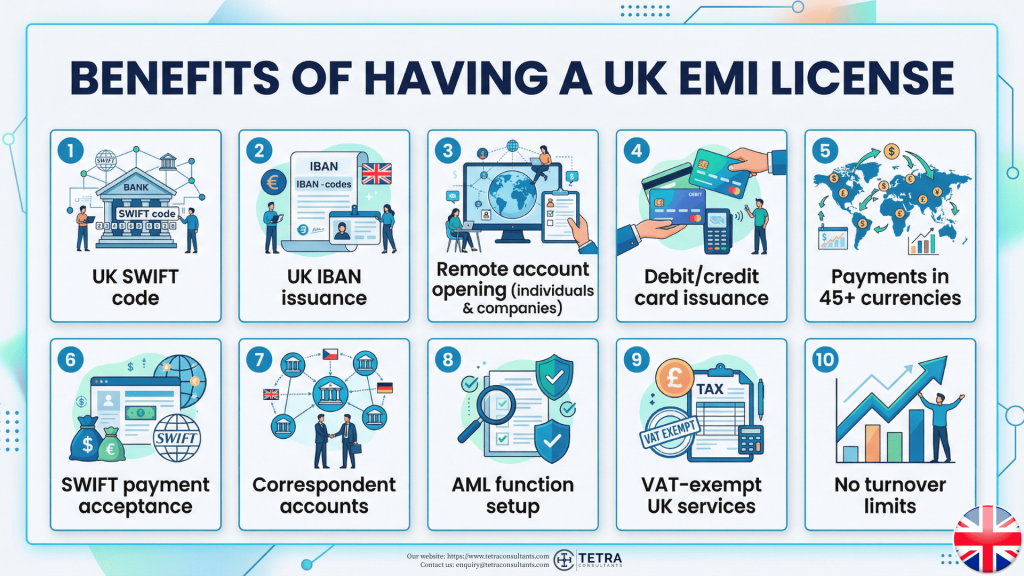

What are the benefits of having a UK EMI license?

As an authorised EMI you will have the following benefits:

- You will acquire an English SWIFT code for transactions

- You will be able to issue English IBAN accounts for your clients

- You will be able to register accounts remotely for individuals and companies

- You will be able to issue credit and debit card payments linked to your customer accounts

- Your company will be able to perform bank payments in more than 45 currencies worldwide

- You can accept payments from all international accounts that use the SWIFT system

- Create correspondent accounts in different countries

- Establish an AML function

- Your financial services are VAT-exempt in the UK

- No restrictions regarding the turnover of the company

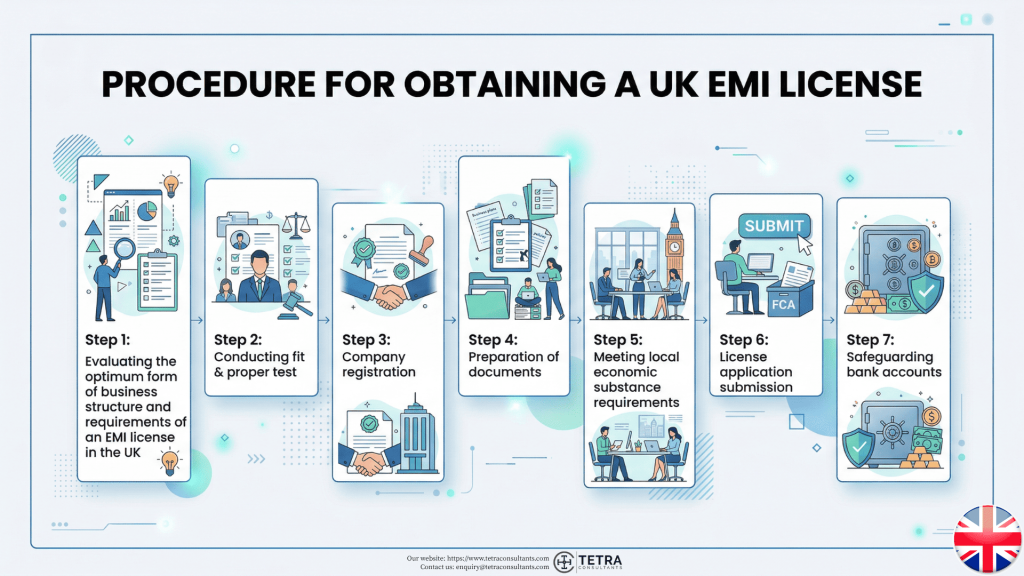

What is the procedure for obtaining a UK EMI license?

The procedure to set up an electronic money institution may vary depending on the amendments taking place in the local laws and regulations. Tetra Consultants has summarized the most prevalent steps that take place during the normal engagement of attaining the EMI license.

Step 1: Evaluating the optimum form of business structure and requirements of an EMI license in the UK

- Tetra Consultants’ team of lawyers and licensing specialists will advise you on the most appropriate form of entity and license for your business based on your projected business operation.

- Prior to the commencement of the engagement in the jurisdiction, our team of specialists will present you with the licensing requirements, including eligibility criteria, paid-up capital requirements, local economic substance requirements, timelines, and procedures.

Step 2: Conducting fit & proper test

- Our team of lawyers and licensing specialists will make sure that every key managerial personnel engaged has the requisite qualifications and is competent enough to take the position, by verifying the informational data and supporting documents for the same.

Step 3: Company registration

- Our lawyers and licensing specialists will perform due diligence on the company’s directors and shareholders. We will move to register the entity with the local Companies Registry after we have all KYC credentials, incorporation forms, and power of attorney.

- We will send the corporate documents, including the Certificate of Incorporation, Memorandum and Articles of Association, and other administrative documents, after the business has been properly registered.

- Additionally, our accounting and tax team, along with our accountant, can help you comply with various regulations to make sure that your business remains fully compliant with laws.

Step 4: Preparation of documents

- The legal experts at Tetra Consultants will draft the necessary documentation for the licensing application. Depending on the other local laws, these papers will contain the business plan, AML/CFT policy, and other necessary documents.

- Tetra Consultants will deliver you the draft of such documents after they have been prepared. Following that, we will email them to you for e-signature and start working on your license application.

Step 5: Meeting local economic substance requirements

- If the local regulator needs you to have economic substance, Tetra Consultants will assist you in meeting those requirements. Our staff will help with the recruitment of skilled local individuals to join the team.

- Tetra Consultants HR team will undertake the applicant shortlisting and initial interview. Following that, you may narrow down the final list of prospects to choose who is most suited to join the team. Tetra Consultants will assist with the preparation of an employment contract with the agreed terms and conditions once the candidate has been approved.

- In addition, our staff will compile a list of physical offices and deliver it to you. We will provide crucial factors such as monthly rental, location, size, and so on so you can better pick which is best for you. Our legal experts will then draft the lease agreement to be signed between you and the landlord after the office has been selected.

Step 6: License application submission

- Once the above is completed, Tetra Consultants will submit the application to the local regulator. Depending on the jurisdictions, you may be required to attend an interview with the regulator prior to license approval. In this case, Tetra Consultants will prepare you for the interview and assist with the follow-up actions required by regulatory authorities.

- All going well, your firm will receive the UK EMI license and will be required to start business operations within the stipulated timeframe in order to maintain the license.

Step 7: Safeguarding bank accounts

- To obtain an EMI license, you will need specialist banking facilities, such as client safeguarding accounts, and access to payment systems, such as IBAN and SWIFT. Furthermore, you will require systems and software to manage your business.

- Corporate bank account opening services through our experts will help you by arranging banking facilities, such as safeguarding accounts, issuing cards, and access to payment infrastructures.

What is the timeline for obtaining a UK EMI license?

Application acceptance

- The FCA, the UK’s regulator, recognizes applications within 7 business days. The application is then allocated to a case officer, who evaluates the information presented and makes a decision.

Decision on an application

- The FCA takes a decision on the application within 3 months of receipt (assuming the FCA has all of the necessary information and documentation), or up to 12 months (if the application is incomplete).

How long does it take to obtain a UK EMI license?

- Prior to the start of the engagement, Tetra Consultants will send you a project plan with the timelines stipulated for company registration, preparation of documents as well as UK EMI license application. This is to ensure that all parties are clear on the upcoming project.

Can the UK EMI license be revoked and canceled?

Yes, the regulatory authority that is FCA can revoke and cancel a firm’s authorization and registration in the form of a UK EMI license:

- If your entity no longer meets the minimum standards;

- If your entity can no longer fulfil its basic regulatory obligations, such as paying fees or submitting returns;

- If your entity can no longer meet its liabilities as they fall due, or where a firm fails to pay the amount due to a consumer under a final decision of the Financial Ombudsman Service (FOS).

Our Services

- Tetra Consultants works as your advisor and trusted partner in your business expansion and payment license application. With our own team of lawyers, licensing specialists, compliance team, and accountants, we tell our clients what they need to know, instead of what they want to hear. Most importantly, we are known for being a one-stop solution for our valued clients.

- We will select an optimal form of the company and help to register a business in the UK, will help to prepare all necessary policies and descriptions, a business plan, prepare and verify the correctness of the documents package for the company, shareholders, provide support for the implementation of management requirements.

- Tetra Consultants will assist you with communications with the FCA and government officials throughout the whole course of the engagement.

- In addition, Tetra Consultants can also assist with attaining other offshore financial licenses depending on your long-term business goals.

Find out more!

- Contact us to find out more about how to get a UK EMI license. Our team of experts will revert within the next 24 hours. perts will revert within the next 24 hours.

FAQs

Author

Sharma Prabakaran

Sharma Prabakaran is the Head of International Business Advisory at Tetra Consultants. With over 15 years of professional experience, he specialises in international business setup, accounting and tax advisory, and cross-industry SME engagements. His expertise encompasses end-to-end project management, ranging from company incorporation and corporate bank account establishment to ongoing annual accounting and tax compliance.