Company Registration

3 Weeks

Local Director?

No

Bank Account Opening

4 Weeks

Travel Required?

No

Malta EMI License in 2026

- At Tetra Consultants, our team of lawyers, licensing specialists, compliance professionals, and accountants will assist you in seamlessly obtaining a Malta EMI License in 2026. We provide end-to-end support including Malta company incorporation, preparation and submission of the EMI license application, regulatory compliance advisory, and post-licensing operational support, ensuring your business meets all requirements set by the Malta Financial Services Authority (MFSA). Our experts will also guide you through capital structuring, safeguarding obligations, governance requirements such as the Four Eyes Principle, and AML/CFT compliance to ensure your Electronic Money Institution is fully aligned with Malta’s Financial Institutions Act and EU regulatory frameworks.

- In the present scenario, Malta remains one of the leading fintech jurisdictions within the European Union. Electronic Money Institutions are licensed by the Malta Financial Services Authority (MFSA) and are further subjected to the EU-wide regulatory frameworks like the Digital Operational Resilience Act (DORA) and the Markets in the Crypto-Assets Regulation (MiCA). These frameworks improve the operational resilience, cybersecurity and consumer protection for the fintech companies operating across the European Economic Area.

- Malta was among the first EU nations to enact EMI regulations. Today, Malta is the leader in technology regulation and fintech, having been the first country to implement specific legal frameworks for DLT (blockchain) and cryptocurrencies.

What are the regulations governing a Malta EMI License in 2026?

- Malta Electronic Money Institutions (EMIs), previously regulated under the Banking Act (Chapter 371 of the Laws of Malta) are now regulated by the Financial Institutions Act (Chapter 376 of the Laws of Malta) (the “Act”) and the MFSA Financial Institution Rules (FIR/01 and FIR/03). These rules outline the licensing requirements, prudential safeguards, capital adequacy standards, and ongoing supervision applicable to the Electronic Money Institutions operating in Malta. Regulations issued there under are considered a solid regime for standalone e-Money Institutions. The legislative amendments enacted in April 2011 brought the regulation of EMIs in Malta, previously regulated under the banking regulations, within the remit of the Financial Institutions Act. This essentially provided Maltese EMIs with a milder legislative touch, resulting in a considerably more appealing environment for operators wishing to commence EMI.

- The change in legislation is widely credited with sparking the sector’s expansion and has had significant regulatory and financial ramifications on the current EMI regime, including, among other things, a decrease in the initial capital requirement from €1m to €350,000, an augmentation of the definition of “electronic money” and the range of activities conducted by EMIs, the introduction of safeguarding prerequisites and redemption rules intended to strengthen protection for consumers.

- In addition to the national legislation, Maltese EMIs should adhere with European regulatory frameworks, this includes:

- Payment Services Directive 2 (PSD2)

- Markets in Crypto-Assets Regulation (MiCA)

- Digital Operational Resilience Act (DORA)

- EU Anti-Money Laundering Directives (AMLD)

What does electronic money mean in 2026?

- The term “electronic money” is defined in the Financial Institutions Act to include “magnetically stored monetary value,” which also refers to payment cards and computer hard drives. Accordingly, “electronic money” fits in this definition whether it is kept on a payment device in the possession of the electronic money holder or stored remotely at a server and managed by the electronic money holder through a dedicated account for electronic money and may eventually include payment by mobile phone.

- As per the Third Schedule of the Financial Institutions Act defines an Electronic Money Institution (“EMI”) as “a financial institution that has been licensed in accordance with this Act and authorized to issue electronic money or that holds an equivalent authorization to issue electronic money in another country in terms of the Electronic Money Directive.”

- Accordingly, e-money can be broadly categorized into two types, namely:

- Card or device-based e-money enables users to make modest purchases without using actual currency by utilizing a portable card or electronic device as an e-wallet. Card/device-based e-money is largely acknowledged as having sparked regulatory growth in the sector.

- Server-based e-money has apparently become more popular in recent years, and Server-based e-money is held remotely at a server that can typically be retrieved and controlled by users.

- The Malta Financial Services Authority (MFSA) is responsible for regulating and licensing Electronic Money Institutions (EMIs) in Malta. An EMI is a financial institution that is authorized to issue electronic money and offer payment services. While EMIs may issue debit cards and operate payment platforms, they are not allowed to conduct lending or even other traditional banking activities.

- The MFSA acts as a single regulator for the financial services sector in Malta and supervises the payment system services in Malta under the Financial Institutions Act (‘FIA’) which is the key act transposing the EU Payment Services Directive 2015/2366 (‘PSD2’).

- In addition to the MFSA, Electronic Money Institutions must comply with anti-money laundering regulations supervised by the Financial Intelligence Analysis Unit (FIAU). Licensed EMIs are required to submit suspicious transaction reports, maintain transaction monitoring systems, and ensure full compliance with Malta’s AML/CFT framework.

What are the minimum regulatory requirements for obtaining a Malta EMI License in 2026?

- To obtain a Malta EMI License, an applicant must comply with regulatory requirements related to capital adequacy, governance structure, operational readiness, and safeguarding of client funds as prescribed by the Malta Financial Services Authority.

Minimum capital requirements

- An applicant must maintain a minimum initial capital of €350,000, as required under the Financial Institutions Act and relevant MFSA Financial Institution Rules. In addition, the EMI must maintain own funds equal to at least 2% of the average outstanding electronic money, subject to adjustment based on the risk profile and business model of the institution.

Safeguarding obligations

- Licensed EMIs should adhere with strict safeguarding obligations, ensuring that the customer funds are protected through the segregated accounts or equivalent safeguarding mechanism with reputable financial institutions.

- For Small Electronic Money Institutions, the capital requirements are lower:

- €50,000 where the average outstanding electronic money is below €1 million

- €100,000 where the average outstanding electronic money is between €1 million and €2 million

Physical office

- Applicants must establish a registered head office in Malta, demonstrating sufficient operational presence within the jurisdiction.

Directors and key management roles

- An EMI must appoint qualified management personnel who satisfy the fit and proper requirements of the regulator. Typically, at least two individuals must be locally present in Malta to effectively direct and manage the institution’s operations.

- Key roles generally include:

- Board of Directors – At least two directors responsible for strategic oversight and governance.

- Risk Manager – Responsible for identifying and managing operational and financial risks within the institution.

- Compliance Officer – Ensures the institution complies with applicable regulatory and AML/CFT requirements.

- MLRO (Money Laundering Reporting Officer) – Responsible for monitoring suspicious transactions and reporting to the relevant anti-money laundering authority.

Governance and operational requirements

- Licensed EMIs must maintain adequate internal controls, accounting records, and risk management systems to ensure prudent operation. The regulator will assess whether the institution has sufficient governance arrangements, transparent reporting structures, and effective oversight mechanisms to comply with regulatory obligations.

- The MFSA also evaluates whether the institution can provide sufficient regulatory information and whether the group structure allows for effective supervisory oversight.

Operational readiness requirements for Malta EMIs in 2026

- Before getting the license approval, applicants should showcase operational readiness, this includes the implementation of compliant fintech infrastructure. This usually includes:

- Cybersecurity frameworks aligned with the DORA requirements

- Secure transaction monitoring tools for the AML detection

- Internal risk management and compliance monitoring systems

- Core banking software that is capable of issuing and managing electronic money

- Payment processing infrastructure with SEPA and SWIFT integration

- EMIs may get Direct SEPA access through the partnerships with licensed financial institutions or use Sponsored/Indirect SEPA access through the intermediary banks.

What are the activities allowed under a Malta EMI License in 2026?

Along with the issuance of e-money a Maltese Licensed EMI may engage in other activities, such as payment services which are regulated under the Second Schedule of the Financial Institutions Act. Such activities include:

- Provision of services allowing cash to be placed on a payment account as well as all the operations required for operating a payment account;

- Provision of services allowing cash withdrawals from a payment account as well as all the operations required for operating a payment account;

- Execution of a money transaction, including transfers of funds on a payment account with the user’s payment service provider or with another payment service provider

- Processing of direct debits, including one-off direct debits

- Processing of payment transactions through a payment card or similar device

- Processing of credit transfers, including standing orders;

- Issuing and/or acquiring payment instruments;

- Money remittance;

- Completion of a money transaction in which the payer’s assent to the money transfer is communicated via any telecommunications, digital, or IT devices, and the payment is made to the controller of the telecommunications, IT system, or network, functioning merely as a middleman on behest of the user of the payment service and the provider of the goods and services;

- Payment initiation services;

- Account information services (AIS);

- Operational and intently associated ancillary services like ensuring monetary transactions completion, foreign exchange services specifically related to payment services, safekeeping activities, and the storage and processing of data, as well as business activities other than the provision of payment services; and

What are the benefits of obtaining a Malta EMI License in 2026?

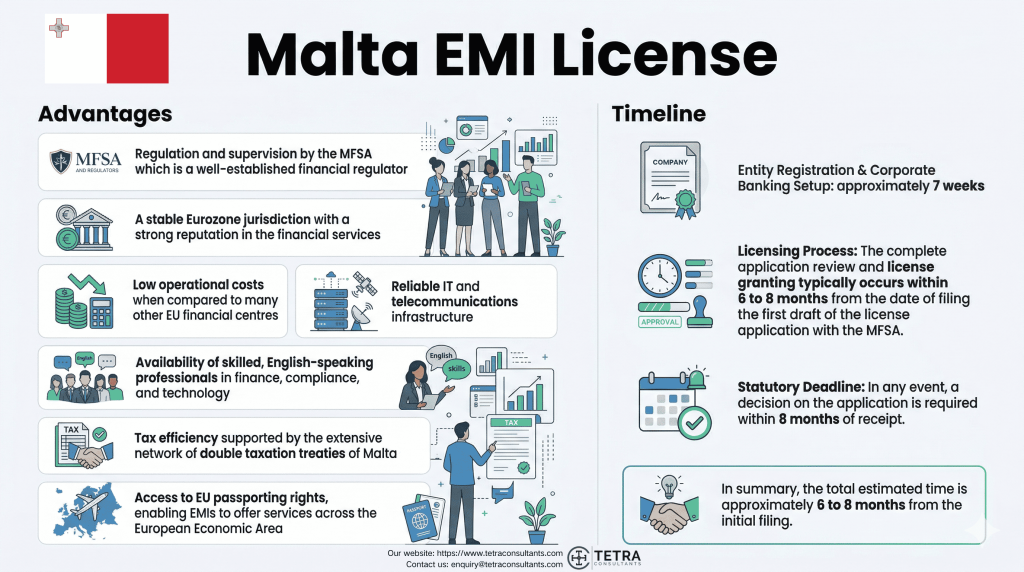

- The main benefits of getting a Malta EMI License in 2026, includes:

- Regulation and supervision by the MFSA which is a well-established financial regulator

- A stable Eurozone jurisdiction with a strong reputation in the financial services

- Low operational costs when compared to many other EU financial centres

- Reliable IT and telecommunications infrastructure

- Availability of skilled, English-speaking professionals in finance, compliance, and technology

- Tax efficiency supported by the extensive network of double taxation treaties of Malta

- Access to EU passporting rights, enabling EMIs to offer services across the European Economic Area

Malta’s full imputation tax system

- Malta operates under a Full Imputation Tax System which enables shareholders to claim the tax refunds on distributed corporate profits. This mechanism has reduced the effective corporate tax burden to approximately 5% for non-resident shareholders, which makes Malta one of the most tax-effective jurisdictions for financial institutions that are operating in the EU.

Small Electronic Money Institution License

- Subject to the satisfaction of conditions stipulated below, the MFSA has the authority to grant authorization to an applicant for registration/recognition as a “small electronic money issuer” thereby waiving the application of all or part of the provisions relating to general prudential requirements, initial capital, own funds, and safeguarding requirements, as set out in the Financial Institutions Act and the applicable MFSA Rules.

- Small EMIs, are defined as companies

- Whose head office is in Malta; and

- That issue electronic money in Malta; and

- The total business activities of the institution generate an average outstanding electronic money that does not exceed two million euros (€2,000,000), and

- None of the natural persons responsible for the management or operation of the business has been convicted of offenses relating to money laundering or terrorist financing or other financial crimes

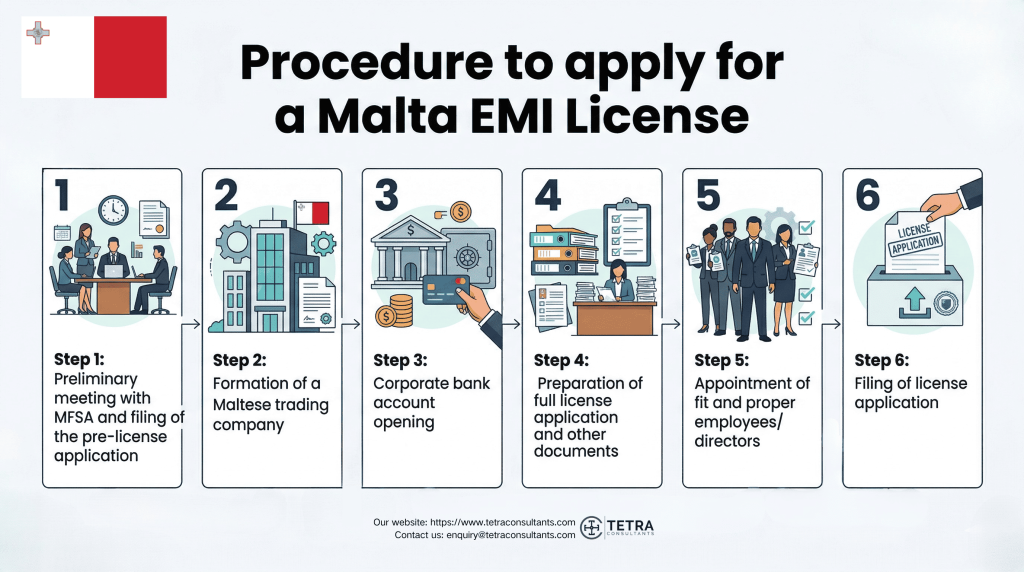

What is the procedure to apply for a Malta EMI License in 2026?

Tetra Consultants’ team of licensing experts recommends going through the steps below in order to understand the typical procedure for applying for a Malta EMI License.

Step 1: Preliminary meeting with MFSA and filing of the pre-license application

- Tetra Consultants will arrange a preliminary meeting with the MFSA to present the proposed business model of the applicant and planned EMI activities. At this stage the basic due diligence documents of shareholders, directors, and main personnel should be submitted.

- The MFSA will begin its fit and proper assessment of the management team, reviewing their experience, competence, and reputation. Relevant individuals will be required to complete personal questionnaires and provide supporting documentation.

- Following the review, the MFSA may grant in-principle approval, subject to certain conditions that must be fulfilled before the full EMI license is issued.

Step 2: Formation of a Maltese trading company

- Once the in-principle approval is granted, Tetra Consultants’ legal team and licensing specialists will assist with the incorporation of a Maltese company suitable for the EMI application. Our lawyers and licensing specialists will then prepare the incorporation documents this includes the memorandum and articles of association, and coordinate notarization wherever required. Once finalized the documents will be submitted to Malta Business Registry for company registration.

- Once registered we will courier the certificate of incorporation and other corporate documents to the address provided.

Step 3: Corporate bank account opening

- To operate as an EMI, the company must open a corporate bank account with safeguarding facilities and access to payment systems such as IBAN and SWIFT.

- Tetra Consultants will assist with corporate bank account opening with reputable banking partners and help arrange safeguarding accounts and payment infrastructure required for EMI operations.

Step 4: Preparation of full license application and other documents

- Our team of lawyers and licensing specialists will prepare the full EMI license application and supporting documents required by Maltese regulations.

- These typically include the business plan, AML/CFT policies, financial projections, and documentation demonstrating the operational infrastructure required to conduct EMI activities. Our accounting and tax team will assist in preparing the financial statements and ensuring they comply with the regulatory and reporting standards required by the MFSA.

- Once finalized, the documents will be submitted for your review and signature before filing the application with the MFSA.

Step 5: Appointment of fit and proper employees/directors

- To meet regulatory substance requirements, the EMI must appoint qualified directors and key management personnel.

- Tetra Consultants will assist with appointing suitable directors and key officers. Furthermore, our experts will also support the setup of operational and administrative requirements, including office arrangements where necessary.

- All key personnel must satisfy the MFSA’s fit and proper criteria before the license application proceeds.

Step 6: Filing of license application

- Once all requirements are fulfilled, our lawyers and licensing specialists will submit the EMI license application to the MFSA.

- The regulator may request additional documents or interviews during the review process. Our team will assist with responding to regulatory queries and preparing you for any required meetings.

- Upon approval, the company will receive the Malta EMI License and may begin operations within the timeframe specified by the regulator.

Malta EMI License and MiCA regulation

- With the implementation of the Markets in Crypto-Assets Regulation (MiCA), an EMI license can act as a regulatory gateway for fintech firms that want authorization to issue Electronic Money Tokens (EMTs) within the EU.

- Several crypto asset businesses establish an EMI structure in Malta in order to support stablecoin issuance, digital wallets, and regulated payment infrastructures that is aligned with the MiCA requirements.

Timeline and cost to obtain a Malta EMI License in 2026?

- The time taken by Tetra Consultants to register a Malta trading company and open a corporate bank account is 7 weeks. In the case where the application filed does not comply with the requirements prescribed in the law, the Authority will determine the application within 3 months of compliance therewith. In any event, an application shall be determined within 8 months of its receipt.

- All in all, the complete application is reviewed and the license is usually granted upon MFSA approval within 6 to 8 months from the date of filing the first draft of the license application.

- While the total cost of obtaining a Malta EMI License is determined by the wide range of services that you require from Tetra Consultants. An EMI license holder in Malta is also required to pay an annual supervision fee equivalent to 0.0002 of the total assets as reported by the license holder in the statutory schedules under applicable Financial Institutions Rules and pertaining to the year immediately before the year when the fee is payable. In any case, such a supervision fee may not be less than €2,500.

- Before we begin the licensing process, we will go through the complete engagement fee with you in full so that you understand exactly what you are paying for. Tetra Consultants strives to be transparent about engagement fees before beginning any engagements. All of these terms and conditions will be properly mentioned in our appointment letter.

Looking to apply for a Malta EMI License in 2026?

- Tetra Consultants works as your advisor and trusted partner in your business expansion and payment license application. With our own team of lawyers, licensing specialists, compliance team, and accountants, we tell our clients what they need to know, instead of what they want to hear. Most importantly, we are known for being a one-stop solution for our valued clients.

- Contact us to find out more about how to get a Malta EMI License. Our team of experts will revert within the next 24 hours.

FAQ

Author

Sharma Prabakaran

Sharma Prabakaran is the Head of International Business Advisory at Tetra Consultants. With over 15 years of professional experience, he specialises in international business setup, accounting and tax advisory, and cross-industry SME engagements. His expertise encompasses end-to-end project management, ranging from company incorporation and corporate bank account establishment to ongoing annual accounting and tax compliance.